Commodity Monthly Monitor

Commodities to catch an inflation bid?

Although commodities as a group pulled back 1.1% last month, it was mainly on the back of natural gas and aluminium prices dropping. Both commodities had astronomical gains earlier in the year and are still up 88% and 35% respectively over the past year.

We believe that the current elevated inflation environment will be positive for the commodity complex. US consumer price index (CPI) inflation rose 6.2% in October 2021, marking the highest level of inflation since 1990. The print, released on Wednesday 10th November 2021, outstripped the Bloomberg consensus survey of 5.9%. The fact that the market keeps being surprised by inflation indicates that something is missing from market expectations. We believe that supply-side shocks are both larger and more persistent than the market had expected. Tell-tale signs of supply bottlenecks are littered through the details, including elevated energy and autos prices.

Commodities are uniquely well-positioned to hedge against unexpected inflation. Commodities have the strongest inflation beta of all major asset classes. Moreover, this beta with unexpected inflation is even higher than the beta with expected inflation. If the drivers of inflation today are unexpected, then commodities are the place to turn to.

The October inflation print (released on 10 November) was enough to even inject some life back into gold. For most of this year, gold has disappointed as an inflation hedge. Our internal forecast models indicate that with this strength of inflation, gold should be trading closer to US$2,300/oz, yet the metal has been trading in a range of US$1730-1830/oz for most of the past 5 months. The October inflation print helped gold push past US$1860/oz for the first time in five months. Gold’s gains were impressive as it was running against the grain of an appreciating US dollar and rising Treasury yields (both of which are normally negative for gold).

We believe the US dollar is appreciating as markets are expecting the Federal Reserve to be pressured to act faster on inflation given the recent surprises. Even though the Federal Reserve has been at pains to communicate that its interest rate hike decision and bond buying tapering decision are separate, the futures markets are pricing in faster rate hikes following the inflation data release. If the Federal Reserve is able to raise rates faster than other central banks, it will increase their interest rate differentials and thus be dollar positive. US dollar strength is normally negative for commodities, but the extent of inflation strength, especially from unexpected sources, may support the complex.

Other short-term risks to commodities include visible slowing down of growth in China. Following the Evergrande debacle, a pullback in the real estate sector in China could have a notable impact on commodity demand. However, we expect any pullback to be temporary in nature and therefore great entry points into the commodity market which is likely to see strong medium-term growth on the back of improving infrastructure demand elsewhere around the globe and an energy transition that will be particularly supportive for base metals and constrain hydrocarbon production.

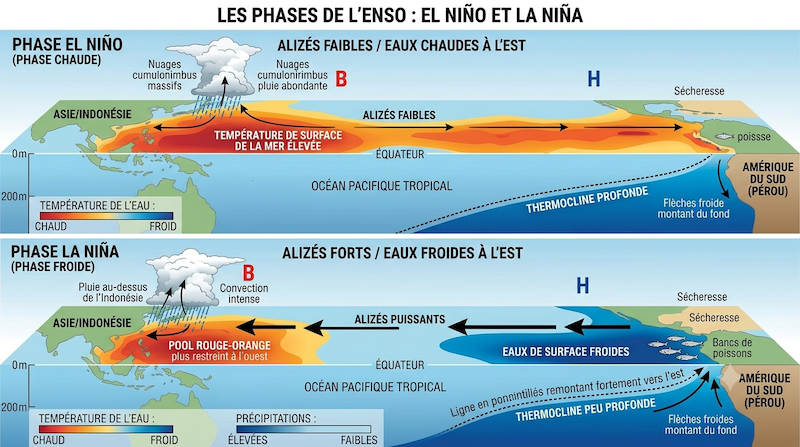

- Agricultural commodities brace for the higher probability of La Niña over the winter. The probability of a La Niña weather pattern developing this year has been increased to 90% by the US National Oceanic and Atmospheric Administration (NOAA). A La Niña can make some places cooler and wetter than normal and other places drier and warmer than normal. Based on our analysis, a La Nina could provide an upside price boost for wheat, corn, and soybeans.

- Seasonal normalisation of US inventory has pressured natural gas prices lower, dragging the energy complex lower. However, natural gas still trades significantly above its 200-day moving average and the threat of supplier shortages in other parts of the world are likely to keep US natural gas prices elevated.

- A month of two halves as the crunch in energy markets hits industrial metals. While the sector returned a large proportion of its first half gains in the second half of October, the only detractor in the end was aluminium while the remaining commodities in the sector ended the month on a positive note.

- Precious metals receive a refreshing reprieve. With US inflation hitting its highest level since 1990 and the Federal Reserve not yet talking about raising interest rates, gold finally appears to be finding the support from inflation it has been searching for several months. Strength in gold seems to be lifting the entire precious metals basket despite the industrial challenges facing platinum and palladium.

Retrouvez l’ensemble de nos articles Business ici

Recommandé pour vous

Les arguments en faveur des stratégies de crédit «crossover» à duration courte

BIT Capital : l’infrastructure IA à l’aube d’une nouvelle vague de croissance

Quand la technologie rapproche au lieu de diviser

Ce qu’El Niño implique pour les matières premières agricoles en 2026

L’IA, moteur de l’avenir – Le marché des cryptomonnaies reste en phase de transition

L’IA en médecine : une promesse tenue?